A reader recently asked a thought-provoking question about the current state of the housing market and its implications for investment.

In a recent episode, a chart was shared illustrating that nationwide housing prices in the U.S. have rarely experienced a decline. This prompted the reader to wonder if now is a good time to buy a house, considering prices are at a high point. The reader, aged 29 and looking to purchase their first home with their spouse, is seeking guidance on how to approach this decision from an investment perspective, acknowledging that there are also non-investment reasons to buy a house.

The dilemma posed by this question can be summarized as follows: the housing affordability crisis, which has been exacerbated by a decade’s worth of gains being realized within a mere 3-year window, raises concerns about the investment potential of buying a house at current prices.

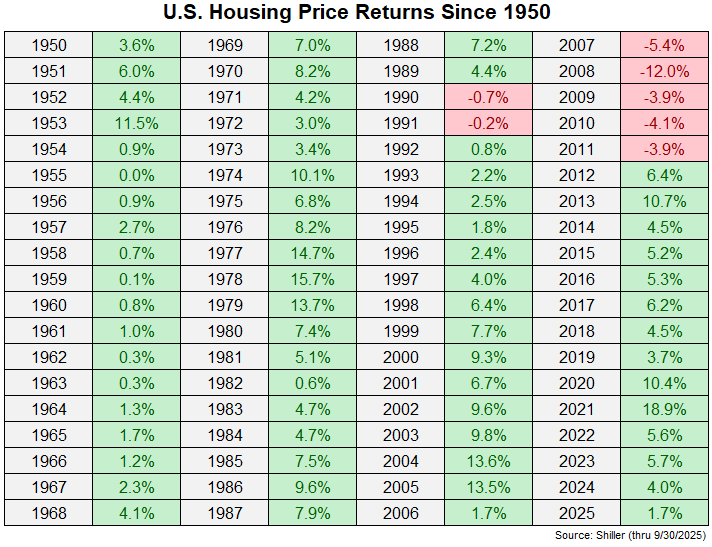

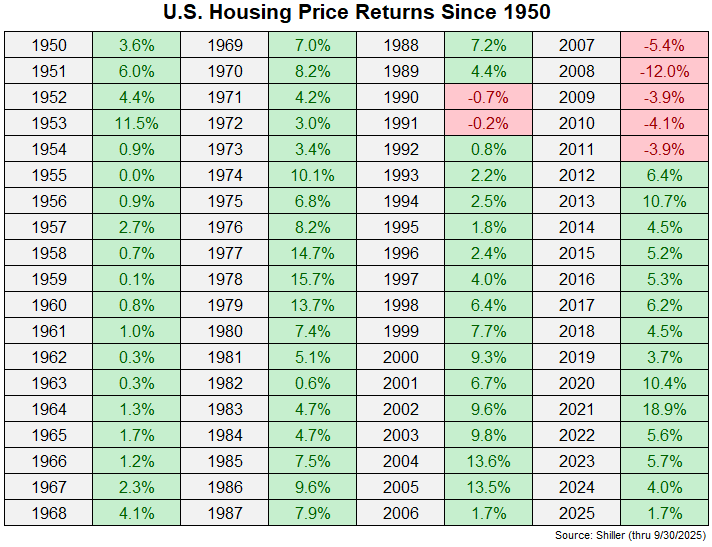

Historically, housing affordability has been a challenge, but housing prices have rarely decreased on a national level. A previously mentioned blog post includes a chart that supports this observation:

The key consideration here is how to reconcile current market data with historical trends. Should investors focus on present market conditions or historical patterns?

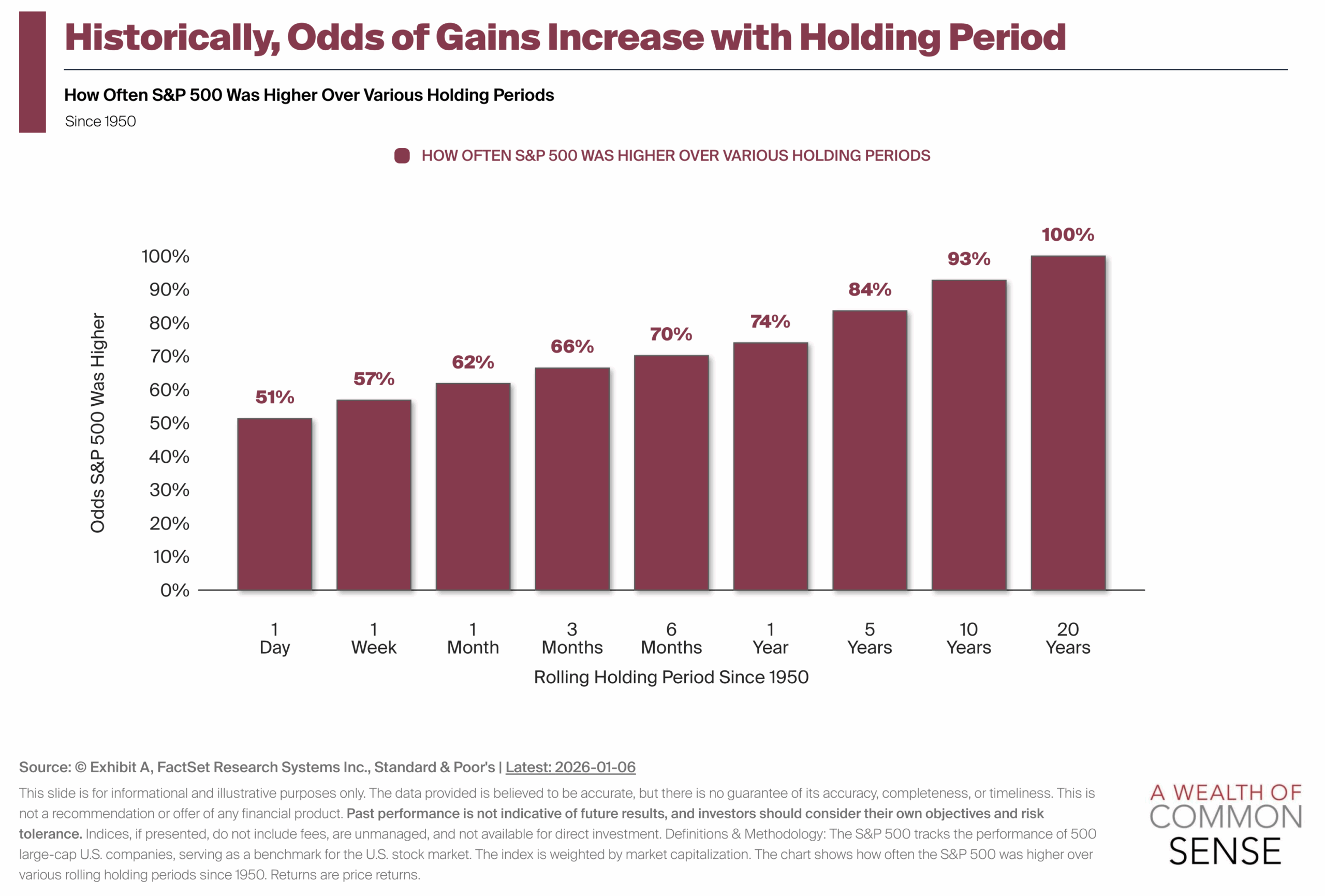

As with any investment, the time horizon plays a crucial role. The longer the investment period, the higher the likelihood of a positive return. This principle is illustrated by a favorite chart examining the win rate for the stock market based on holding periods:

The stock market, often likened to a casino, presents a unique scenario where the longer you invest, the higher your chances of emerging victorious.

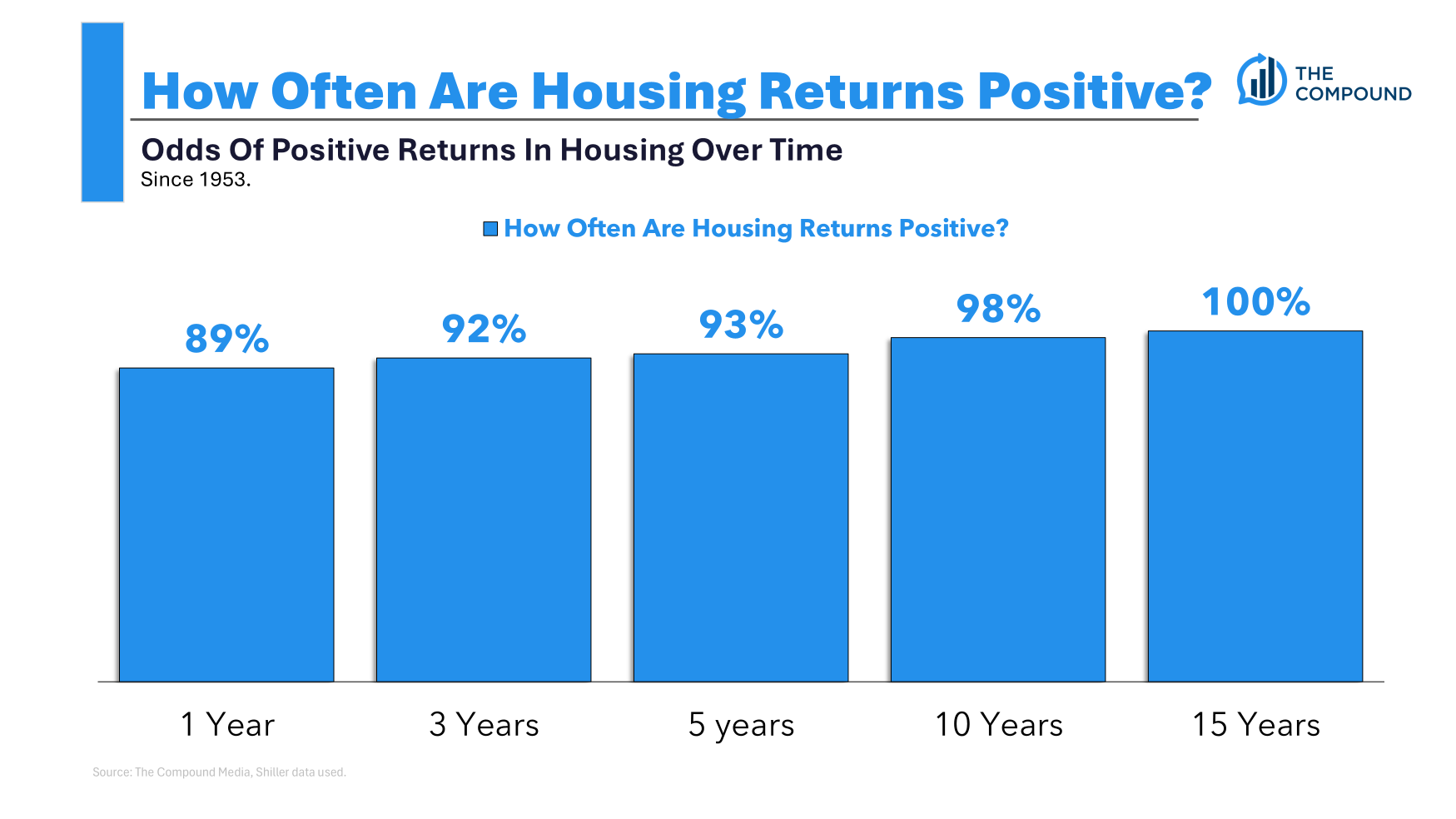

A similar analysis for the housing market, dating back to the 1950s, reveals an impressive win rate across various holding periods:

While the expected returns in the housing market are generally lower and less volatile than those in the stock market, these results align with theoretical expectations and practical observations.

It’s essential to consider the ancillary costs associated with homeownership, such as realtor fees, property taxes, closing costs, insurance, and maintenance. These costs underscore the importance of a longer time horizon in the housing market, as they can significantly erode potential gains if you’re frequently buying and selling properties.

Given the uncertainty surrounding future housing prices, it’s challenging to predict what will happen next. It’s possible that prices might stagnate for a few years as incomes catch up, or they could continue to rise in line with inflation. Alternatively, inflation and demographic changes could drive housing prices even higher.

The 2020s serve as a prime example of the unpredictability of housing price returns, with the pandemic-induced boom being an unforeseen event.

In the absence of a crystal ball, here are some key considerations for those concerned about the investment aspect of buying a house in the current environment:

Using a smaller down payment could be a viable strategy. If you’re apprehensive about housing as an investment, you might opt for a 5-10% down payment instead of 15-20%. This approach involves borrowing more but requires less upfront capital in an asset that might struggle in the coming years, allowing you to retain more money in other risk assets.

Skipping the starter home is another option. The costs associated with real estate transactions, such as realtor fees and closing costs, can be substantial. Investing in a more permanent home that you can see yourself living in for an extended period might be a preferable strategy, as it minimizes the need for frequent buying and selling.

Living in the house longer can also be beneficial. By lengthening your time horizon, you can ride out potential short-term market fluctuations. If you plan to live in the house for 10+ years, the investment potential is likely to improve.

The most critical factor is your ability to service the mortgage debt and manage the ancillary costs of homeownership. If you can achieve this while living in your desired neighborhood and derive psychological benefits from homeownership, then it’s likely worth considering.

This question was addressed in a recent episode of Ask the Compound:

Bill Sweet, my favorite CFO, joined us on the show to discuss topics like Roth 401ks, using margin in your portfolio, balancing retirement accounts, and how a 22-year-old should save for retirement. We also explored various tax questions to prepare for the new year.

Further Reading:

Will Home Prices Finally Fall in 2026?

1Assuming your financial institution allows it.

2It was also the maximum we could afford at the time.