President Trump’s latest salvo against Fed Chair Jerome Powell called for 1% interest rates.

And he added that he’d “love him to resign if he wanted to, he’s done a lousy job.”

Thing is, if the Fed were to cut its own fed funds rate to 1%, how would that actually affect mortgage rates?

There’s not a clear correlation between the short-term FFR and the long-term 30-year fixed.

So there’s no guarantee Powell’s replacement, if he/she were to lower rates aggressively, would lead to lower mortgage rates too.

Trump Wants 1% Interest Rates and a Powell Resignation

The President told reporters that “I think we should be paying 1% right now, and we’re paying more because we have a guy who suffers from, I think, Trump Derangement Syndrome.”

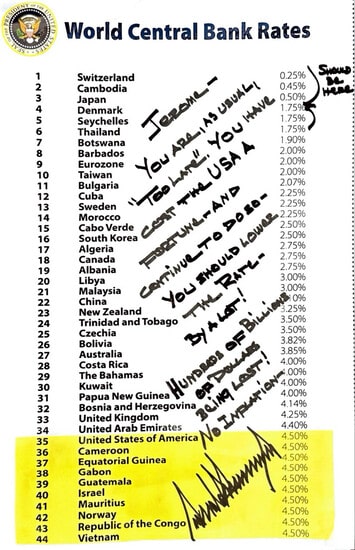

He also posted this image on his Truth Social account saying rates should be in the 1% or less range.

This isn’t the first time Trump has called on Powell to lower rates, nor will it be the last, but I found it interesting he explicitly asked for 1% rates this time around.

To put that in perspective, the FFR is currently at a range of 4.25% to 4.50%.

It was effectively set at zero from 2009 to 2015, and again during the pandemic, before rising above 5% to combat out-of-control inflation.

Last year, the Fed cut its key policy rate 100 basis points (bps) via four rate cuts, but has since taken their foot off the pedal.

Trump and FHFA President Pulte have both been pressing Powell to keep cutting, with their critique of his job as Fed boss growing louder and louder.

Thing is, the Fed doesn’t control mortgage rates. You could lower the FFR without seeing a meaningful change in mortgage rates.

Any cuts need to be a warranted in order for bond yields to come down. And it is the 10-year bond yield that correlates with long-term mortgage rates.

So while the Fed could start aggressively cutting again with a Powell replacement, the bond market might not respond as Trump and Pulte expect.

Really, the only way to forcibly bring back record low mortgage rates, or at least markedly lower mortgage rates, would be via direct Fed intervention.

This means another round of QE, where the Fed buys mortgage-backed securities (MBS) to increase prices and bring down associated yields (interest rates).

But the chance of that remains slim, at least at this juncture. Though you can’t rule anything out if the housing market continues to stall as it has.

Interest Rates at 1% Would Lower HELOC Rates Significantly

When it comes down to it, the only guarantee you get from a Fed rate cut is a lower prime rate, because they move in lockstep.

The prime rate is historically priced around 300 bps (3%) above the fed funds rate. This spread is constant, so if the FFR goes down by 25 bps, the prime rate goes down by 25 bps too.

It’s currently at 7.50%, while the FFR is 4.25% to 4.50%, so if the Fed somehow agreed to cut their rate to 1%, you’d have prime at 4%.

That’d be great news for homeowners with HELOCs, which are priced based on the prime rate.

Whenever prime goes down, so too do HELOC rates. So that would result in big savings for those with HELOCs.

They’d see their interest rates drop about 350 basis points (3.5%), which would obviously result in a massive decrease in monthly payment in the process.

But the 30-year fixed could be a different story entirely. If the bond market doesn’t like the Fed rate cuts, perhaps because they feel forced, they might not react as expected.

Same with MBS investors. So any great plan to lower mortgage rates and give the housing market a boost might not come to fruition.

However, if the economy does continue to show signs of slowing, with falling inflation and rising unemployment, bond yields should theoretically come down as well.

In that case, you’d get a lower 30-year fixed mortgage as well, but that wouldn’t really be due to the Fed.

It’d be driven by the economic data, which ironically is what drives Fed policy decisions in the first place.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.